Key Takeaways:

- D&O insurance is meant mainly to protect company executives and board members against claims resulting from their actions related to running a business.

- All businesses face the risk of lawsuits against their directors and officers—even small companies, which may not have a lot of cash to defend against claims.

- Think holistically about safeguarding your assets and the role D&O insurance might play in your broader asset protection plan.

As a successful entrepreneur, you and the key people around you make the business decisions that drive your company—hopefully in an upward direction!

However, some decisions don’t turn out well, which can result in lawsuits that may be costly, both financially and emotionally.

The good news: There are many ways to protect yourself.

One of the more cost-effective approaches for many entrepreneurs is to have directors and officers (or D&O) insurance. Here’s a look at this powerful type of insurance—and how it might help safeguard you and your most important business and personal assets.

Why executives purchase D&O coverage

D&O insurance is liability coverage for company executives and board members, meant mainly to protect them from claims that result from their actions in running the business. It can also reimburse the company if it has to pay out claims in order to protect the directors and officers (see Exhibit 2).

The appeal of D&O insurance coverage is clear: Company directors and officers are human beings who can, and do, make mistakes. When that happens, they might be personally liable for any adverse consequences because of those errors in judgment. Considering that many businesses are operating in increasingly complicated environments, that compliance is a bigger concern now than in the past and that plaintiffs are more aggressive than ever, the probability of companies being sued because of the actions of their executives is elevated.

Indeed, the number of class-action securities suits filed increased steadily each year from 2013 through 2019, before dipping during the pandemic.

These are a few of the reasons directors and officers might be sued:

- Breach of fiduciary duty

- Misrepresenting company financials

- Misusing company funds

- Noncompliance with workplace laws

Example: A company’s directors misrepresent the firm’s financial status in order to win a big contract. The customer later sues when it’s discovered the company lacks the assets needed to meet the contract’s requirements.

In addition, emerging and growing risks are fueling interest in D&O insurance. Such risks include issues around ESG—environment, social and governance—concerns, as well as cyberattacks and whether business leaders are taking the necessary steps to protect their companies’ digital assets. It’s also possible that we could see more suits involving pandemic-related disruptions.

What’s more, mistakes don’t always result from reckless behavior. Even when company directors and officers are diligent and thoughtful, they can still make decisions that generate problems for the company or others—problems for which they can be held responsible.

D&O insurance provides financial protection for the supposed “wrongful acts” of directors and officers of a company. Therefore, D&O insurance can help provide a certain degree of confidence and financial security for executives—empowering them to make business decisions without the proverbial sword of Damocles (i.e., financial ruin) hanging over them.

D&O insurance also helps avoid costly, time-consuming and emotionally draining lawsuits, which, as noted, are not exactly uncommon these days. And in the event of a lawsuit, the insurance can enable executives to settle many claims quickly and discreetly.

Often, D&O insurance is used to augment and enhance the indemnification provisions in a firm’s articles of incorporation or bylaws that hold harmless directors and officers for losses due to their decisions.

Mistake to avoid: Many businesses never bother to get D&O coverage because they assume—mistakenly—that they’re protected by their other insurance (such as an umbrella policy). However, other policies generally don’t address management errors.

Warning: Don’t assume you don’t need D&O insurance if your company is private and/or relatively small. All businesses face the risk of lawsuits against their directors and officers—and a small business lacking a large war chest of cash might need D&O protection as much as the biggest business in town.

Limits to D&O coverage

There are specific company-based risks that D&O insurance is most often meant to address. One major area is employment and human resources issues, including sexual harassment and wrongful termination claims.

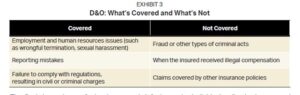

That said, D&O insurance isn’t a shield for any and every action taken by company brass. There are limits to the protections it offers, as summarized in Exhibit 3. Essentially, bad actions that are intentional or already covered by other insurance policies are not covered by D&O insurance.

Important: With D&O insurance policies, claims are covered only if they’re made when the policy is in force (i.e., the policy is currently in effect) or within a stipulated extended reporting period. What’s more, some D&O insurance policies will have a retroactive coverage period, meaning that claims will be paid for wrongful acts committed before the policy was obtained.

Bonus: D&O insurance doesn’t just provide protection. It can also help attract and retain the high-quality talent you may need in order to maximize your success. Top execs and professionals are often wary of joining a firm if their assets won’t be safe from lawsuits.

Three main types of protection

D&O policies can differ from each other, with each having its own specific terms and details. That said, many D&O policies tend to offer three main types of protection for directors, officers and companies:

- Side-A. This covers directors and officers against claims if the company can’t indemnify them. That might be the case if, for example, the company has declared bankruptcy.

- Side-B. Called corporate reimbursement, this helps protect companies that do indemnify their directors and officers. It reimburses costs that companies incur when defending their directors and officers against claims or charges.

- Side-C. This coverage is also known as entity coverage. It helps protect the company itself from claims.

Finding the ‘right’ policy

Selecting D&O insurance can be somewhat tricky. For starters, there’s no foolproof method or rule of thumb for getting the exact “right” amount of coverage.

Example: Business owners commonly look at the average or mean amount of settlement payouts in their industry or geographic area, and choose that amount of coverage. Trouble is, many D&O lawsuit cases are sealed, so the average reported payout may not reflect the actual payouts that aren’t widely known.

That said, it can certainly make sense to factor in considerations such as these:

- Any existing insurance that directors and officers already have that could cover mistakes they make in working with your firm

- The number of directors and officers working with you, and their level of expertise (i.e., Are they professionals in the areas where they will be making decisions, or are they “golf buddies”?)

- Your firm’s financial strength and ability to tolerate financial risks

- The full cost of D&O-related lawsuits—which might include not only the settlement but also the legal fees (which can be enormous, especially in a long, drawn-out case)

D&O insurance as part of an overall asset protection plan

It is often wise for accomplished business owners to think holistically about safeguarding assets and the role of D&O insurance in a broader asset protection plan. These are some other components the asset protection plan might include:

- Personal umbrella policies

- The use of various corporate structures and partnerships

- Placing assets into trusts

The objective for entrepreneurs is to smartly manage some of the risks they are taking and be prepared to deal with certain adverse scenarios when they arise.

Conclusion

If you haven’t already, consider whether D&O insurance would help you reduce a key business risk—and how D&O coverage might work in concert with other financial strategies you may be using to safeguard assets and build wealth.

That said, even if you already have D&O insurance, it may be smart to assess your current coverage and terms to ensure your policy offers the protection you need. That’s especially true if your business, or the industry it operates in, has experienced significant changes. Given the many new challenges we’ve encountered in recent years, it’s likely that now is a good time to give D&O insurance a fresh look.

VFO Inner Circle Special Report

By John J. Bowen Jr.

© Copyright 2023 by AES Nation, LLC. All rights reserved.

No part of this publication may be reproduced or retransmitted in any form or by any means, including but not limited to electronic, mechanical, photocopying, recording or any information storage retrieval system, without the prior written permission of the publisher. Unauthorized copying may subject violators to criminal penalties as well as liabilities for substantial monetary damages up to $100,000 per infringement, costs and attorneys’ fees.

This publication should not be utilized as a substitute for professional advice in specific situations. If legal, medical, accounting, financial, consulting, coaching or other professional advice is required, the services of the appropriate professional should be sought. Neither the author nor the publisher may be held liable in any way for any interpretation or use of the information in this publication.

The author will make recommendations for solutions for you to explore that are not his own. Any recommendation is always based on the author’s research and experience.

The information contained herein is accurate to the best of the publisher’s and author’s knowledge; however, the publisher and author can accept no responsibility for the accuracy or completeness of such information or for loss or damage caused by any use thereof.